Utah's multifamily market presents compelling tax advantages through strategic cost segregation and entity structuring, particularly with permanent bonus depreciation extensions through 2026. Salt Lake City's median multifamily cap rates of 5.8% combined with accelerated depreciation schedules can generate substantial first-year tax benefits for sophisticated investors. Our analysis shows properly executed cost segregation studies on Utah properties averaging 25-35% of basis in accelerated components, translating to $125,000-$175,000 in additional first-year deductions per $500,000 investment. The state's favorable entity tax treatment and lack of personal property tax on business equipment further enhance returns for out-of-state investors seeking geographic diversification.

Utah Multifamily Tax Landscape

Utah's multifamily investment environment offers unique tax advantages that sophisticated investors often overlook. The state's 4.85% corporate tax rate combined with no personal property tax on business equipment creates a favorable foundation for cost segregation strategies.

Bonus depreciation permanency through 2026 allows 100% first-year expensing of qualified components identified through cost segregation studies. In our analysis of Salt Lake County multifamily properties, this typically represents 25-35% of total acquisition cost in accelerated depreciation.

Utah's conformity requirements with federal depreciation elections mean investors can't pick and choose between state and federal bonus depreciation treatment. This all-or-nothing approach requires careful planning but eliminates complex book-tax differences.

The state's net operating loss carryforward provisions allow unlimited carryforward periods, providing flexibility for investors experiencing volatile cash flows during market transitions.

Cost Segregation Study Components

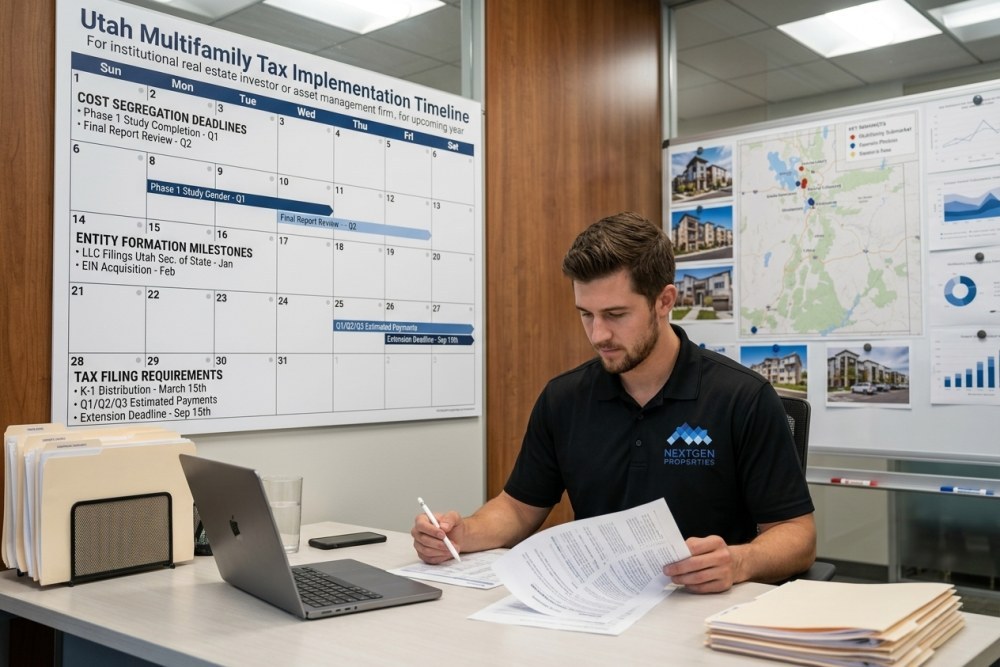

Nearly one-third of Utah multifamily acquisition costs qualify for accelerated depreciation through cost segregation - dramatically improving first-year tax benefits

Utah multifamily properties typically yield substantial personal property components eligible for accelerated depreciation. Apartment complexes built since 2010 average 28-32% of basis in 5, 7, and 15-year property classifications.

Land improvements represent the largest accelerated category in Utah developments. Parking lots, landscaping, and site utilities qualify for 15-year treatment versus 27.5-year residential real property depreciation.

Interior components including appliances, carpeting, and specialized electrical systems qualify for 5-year treatment. Utah's dry climate typically preserves these components longer than coastal markets, but depreciation timing remains identical.

Tenant improvement allowances and common area upgrades completed within 24 months of acquisition may qualify for immediate expensing under Section 179 or bonus depreciation, depending on the specific improvements and timing.

Engineering-Based Studies

Utah requires engineering-based cost segregation studies for properties over $1 million to withstand IRS scrutiny. The state's construction cost databases provide reliable benchmarking for component valuations.

Qualified studies typically cost $8,000-$15,000 for properties under $5 million but generate first-year tax savings of $75,000-$150,000 for investors in higher tax brackets.

The study must be completed by December 31st of the acquisition year to claim maximum first-year benefits, though catch-up adjustments remain available through Section 481(a) filings.

Bonus Depreciation Optimization

Permanent bonus depreciation through 2026 allows immediate expensing of all qualified property identified in cost segregation studies. This creates significant cash flow acceleration for Utah multifamily investors.

The key optimization involves balancing current-year tax benefits against future depreciation recapture exposure. Properties held longer than five years typically benefit from full bonus depreciation election.

AMT implications disappeared with tax reform, eliminating previous restrictions on bonus depreciation timing. Utah investors can now elect bonus depreciation without AMT adjustment concerns.

Mixed-use properties require careful component allocation between residential and commercial spaces, as each follows different depreciation schedules and bonus depreciation eligibility rules.

Timing Elections

Partial bonus depreciation elections allow investors to dial down the percentage of qualified property receiving immediate expensing. This flexibility helps manage taxable income in high-earning years.

Utah's tax year conformity requirements mean partial federal elections automatically apply at the state level. Investors can't elect different percentages for federal versus state purposes.

The election applies to all qualified property placed in service during the tax year, not individual assets. This all-or-nothing approach requires careful year-end planning for multi-property acquisitions.

Entity Structure Strategies

Pass-through entities typically provide better tax efficiency for Utah multifamily investments, particularly when cost segregation generates substantial first-year losses. Single-member LLCs offer the simplest structure for individual investors.

Multi-member partnerships allow flexible loss allocation among partners, enabling high-income investors to absorb larger depreciation benefits while providing lower-income partners with cash flow distributions.

S corporation elections can reduce self-employment tax exposure for active real estate professionals but limit loss pass-through to stock basis plus debt basis. Utah follows federal S election requirements without additional state-level compliance.

C corporation structures rarely optimize multifamily returns due to double taxation, but may benefit investors seeking to retain earnings for future acquisitions or development projects.

Series LLC Considerations

Utah recognizes series LLCs with each series treated as separate entities for liability and tax purposes. This structure works well for investors acquiring multiple properties while maintaining asset protection.

Each series can make independent tax elections, including cost segregation timing and bonus depreciation percentages. This flexibility allows optimization across property types and acquisition dates.

Series LLCs require careful documentation and separate accounting for each series to maintain liability protection. Commingling assets or operations between series can pierce the protective veil.

Salt Lake City Market Dynamics

Salt Lake County represents 65% of Utah's multifamily investment volume, with median cap rates currently ranging 5.6-6.2% depending on submarket and asset class. The market's job growth averaging 3.2% annually supports rental demand.

West Valley and Murray submarkets offer the highest cap rates at 6.0-6.4%, while downtown Salt Lake City properties trade at 5.2-5.8% premiums. Cost segregation benefits apply equally regardless of submarket.

Construction costs averaging $185-$210 per square foot for new multifamily development create substantial land improvement and personal property components eligible for accelerated depreciation.

The market's limited rent control exposure and landlord-friendly legislation preserve cash flow predictability, important for investors modeling long-term depreciation recapture scenarios.

Acquisition Timing

Year-end acquisitions maximize first-year depreciation benefits since cost segregation components receive full-year depreciation regardless of acquisition date. December closings can accelerate tax benefits by 11 months.

Utah's relatively efficient closing process typically requires 30-45 days from contract to closing, allowing investors to plan year-end acquisitions with reasonable certainty.

Properties requiring immediate capital improvements should close by November to ensure improvements qualify for current-year bonus depreciation treatment.

Implementation Timeline

Pre-acquisition planning should begin 60-90 days before closing to ensure proper entity structure and tax strategy alignment. Early planning allows investors to optimize acquisition financing and ownership structure.

Cost segregation studies must commence immediately after closing to meet December 31st deadline for current-year benefits. Most qualified firms require 4-6 weeks to complete engineering analysis and deliver final reports.

Tax return preparation should begin in January to ensure proper depreciation calculations and bonus depreciation elections. Returns claiming large depreciation benefits require additional documentation and review time.

First-quarter estimated tax payments may require adjustment based on accelerated depreciation benefits. Utah requires quarterly estimates when tax liability exceeds $500.

Professional Team Assembly

Cost segregation specialists should hold engineering credentials and demonstrate Utah market experience. Firms lacking local construction cost databases may produce inaccurate component valuations.

Tax advisors must understand both federal and Utah depreciation requirements, particularly conformity rules and NOL carryforward provisions unique to the state.

Legal counsel should specialize in Utah entity formation and real estate tax planning. Generic incorporation services rarely address multifamily-specific compliance requirements.

Compliance and Documentation

Utah tax compliance requires careful documentation of cost segregation components and bonus depreciation elections. The state's conformity requirements eliminate most federal-state differences but create detailed substantiation requirements.

Cost segregation studies must include detailed engineering analysis, component-by-component asset listings, and Utah-specific construction cost benchmarking. Generic studies often fail Utah Department of Revenue scrutiny.

Record retention requirements extend throughout ownership plus the statute of limitations period. Digital document management systems help organize the substantial documentation supporting accelerated depreciation claims.

Annual compliance includes federal Form 4562 depreciation reporting and Utah TC-20 supplemental schedules. Multi-entity structures may require consolidated reporting depending on ownership percentages and elections.

Audit Defense Preparation

IRS audit rates for cost segregation returns average 2-3% annually, making proper documentation essential. Utah typically follows federal audit adjustments but may initiate independent reviews of large depreciation benefits.

Professional liability insurance from cost segregation providers should include audit defense coverage and penalty protection. Most qualified firms provide 3-5 years of audit support as standard service.

Contemporaneous documentation requirements mean investors can't reconstruct cost segregation support after audit initiation. Complete records from closing through study completion provide the strongest defense.

Exit Strategy Tax Planning

Depreciation recapture at 25% federal rates plus Utah's 4.85% rate creates combined 29.85% tax liability on accelerated depreciation benefits. This recapture applies regardless of holding period.

Section 1031 exchanges defer recapture but require like-kind property identification within 45 days and completion within 180 days. Utah's limited exchange inventory may constrain options for larger properties.

Installment sale treatment can spread recapture over multiple years, reducing the tax rate impact for investors in varying annual income brackets. Utah follows federal installment sale rules with minimal modifications.

Charitable remainder trusts and other advanced strategies may eliminate recapture for investors with estate planning objectives, though implementation requires sophisticated tax counsel.

Succession Planning

Stepped-up basis at death eliminates depreciation recapture for heirs, making Utah multifamily attractive for generational wealth transfer strategies. The state's lack of inheritance tax preserves more value than many alternatives.

Grantor trusts can shift future appreciation to heirs while allowing grantors to continue claiming depreciation benefits during lifetime. Utah's trust-friendly statutes support sophisticated planning structures.

Family limited partnerships enable gradual wealth transfer through annual gifting while maintaining operational control over multifamily investments throughout the transfer period.

Frequently Asked Questions